Sales in 2023 to Remain Similar to 2022 Activity

Metro Vancouver home sales set or neared historic records in 2021 and 2022 on both ends of the spectrum. Sales activity hit a record high in March of 2021 and closed 2022 near historic lows after accounting for typical seasonal variation.

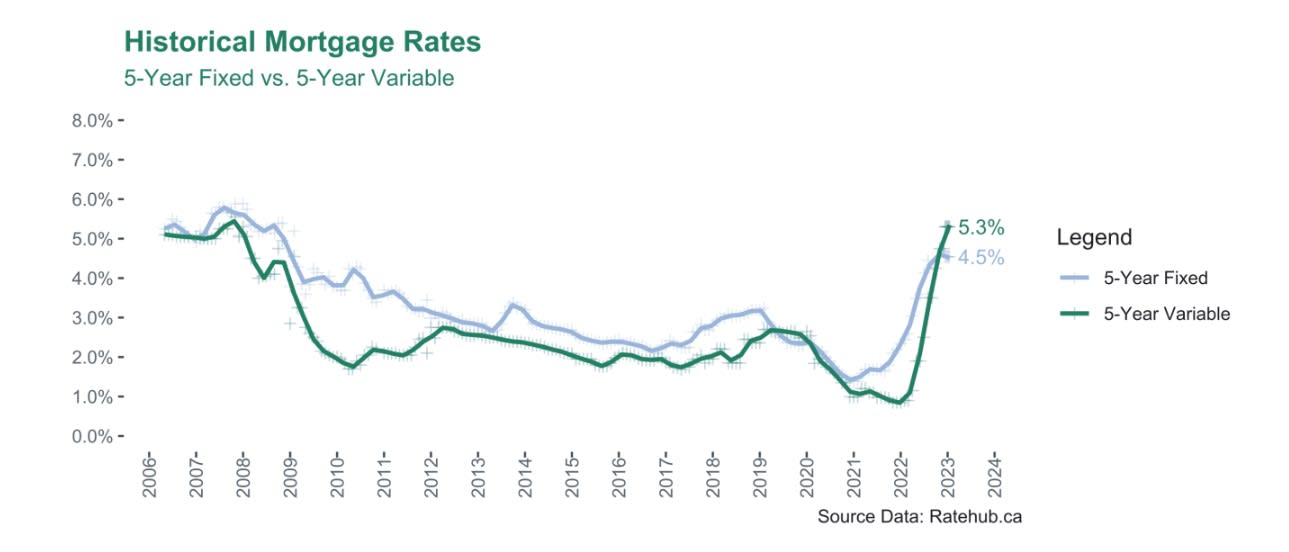

The key economic variable most responsible for this oscillation between extremes has been the spike in mortgage rates, as a result of the Bank of Canada rapidly raising the policy interest rate to quell inflationary pressures not seen in the country in more than thirty years.

At the time of publication, inflation remains stubbornly high, despite the Bank of Canada's historically monumental efforts to bring inflation back to their preferred target range of between one and three per cent. Largely because of this, mortgage rates are expected to remain higher than market participants had been used to in recent times.

Historically, the data indicate that when mortgage rates rise rapidly, sales activity in Metro Vancouver has tended to slow considerably and can take upwards of 24 months to recover to levels seen before the tightening cycle began.

Today’s consensus view among many economists and professional forecasters is that the Bank of Canada is at (or very near) the peak of the current interest rate tightening cycle. Predictions of mortgage rates falling precipitously are few if any, and it is largely against this backdrop that the Real Estate Board of Greater Vancouver (REBGV) forecasts home sales activity to remain below the levels seen in 2021, and roughly in line with 2022 figures across product types.

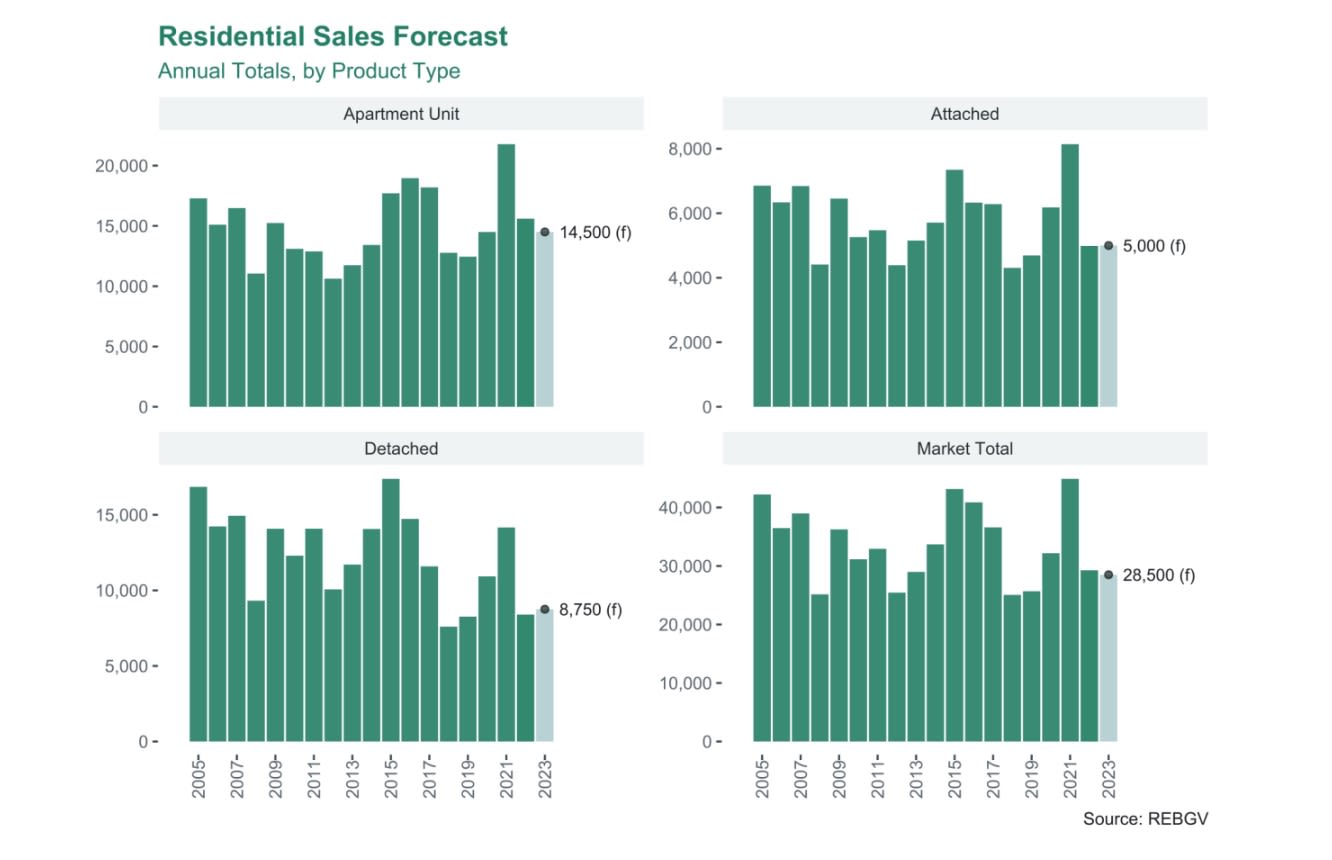

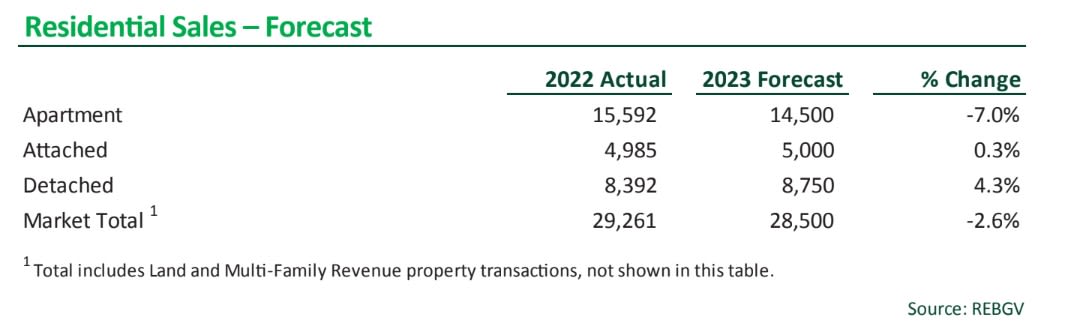

Sales forecast

Sales across Metro Vancouver are expected to reach approximately 28,500 in 2023. This represents a 2.6 percent decrease over the 29,261 sales in 2022.

The table below summarizes our sales forecasts by product type:

Home Prices See Slight Increases in 2023

In percentage terms, rapidly escalating mortgage rates haven’t tended to impact prices as negatively in Metro Vancouver as they have sales activity, historically speaking.

It was only the tightening cycle of the early 1980s, which resulted in a fairly signicant2 price correction in the Metro Vancouver market. Nearly all other historical tightening cycles in Canada yielded more modest declines in prices in the region. Interestingly, a few tightening cycles were even associated with price escalation; a somewhat counterintuitive result that is nonetheless a verifiable fact of the historical record. So far, the current cycle has resulted in prices declining roughly 10% from the beginning of the cycle, with the pace of decline beginning to show signs of slowing.

A key factor that has underpinned prices in the region over the last 40 years has been the steady population increase in Metro Vancouver and surrounding areas. Despite the well-publicized challenges of housing affordability in this region, the number of people who continue choosing to reside here represents an important source of demand pressure that continues to push up against a supply of homes that remains scarce, in relative terms.

With the federal government recently announcing higher immigration targets between 2023 and 2025, and with the best estimates of future population growth available3 suggesting BC and the Vancouver region will continue growing, demand pressure is unlikely to abate significantly, particularly over the long term.

Reconciling this long-term outlook with the near-term, the rapid rise in mortgage rates over the past year has reduced purchasing power and pushed many potential market participants to the sidelines. As the

real estate market continues to adjust to the higher mortgage rate environment, it is likely that more buyers and sellers will step back into the market.

real estate market continues to adjust to the higher mortgage rate environment, it is likely that more buyers and sellers will step back into the market.

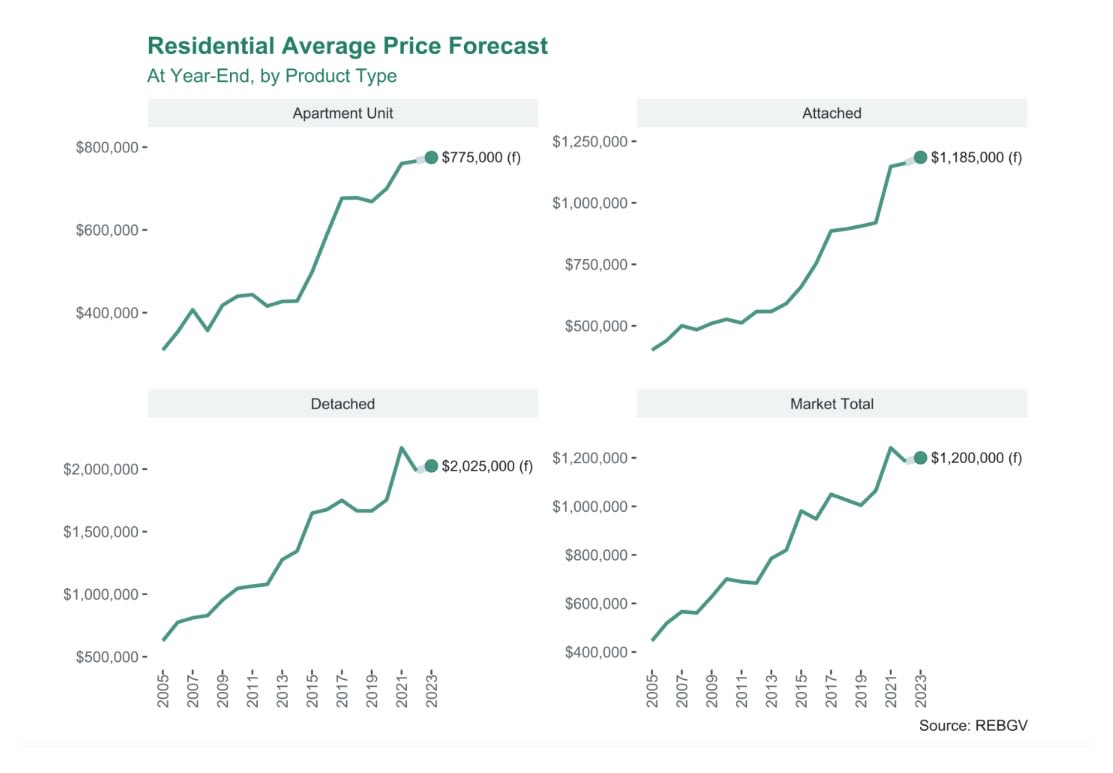

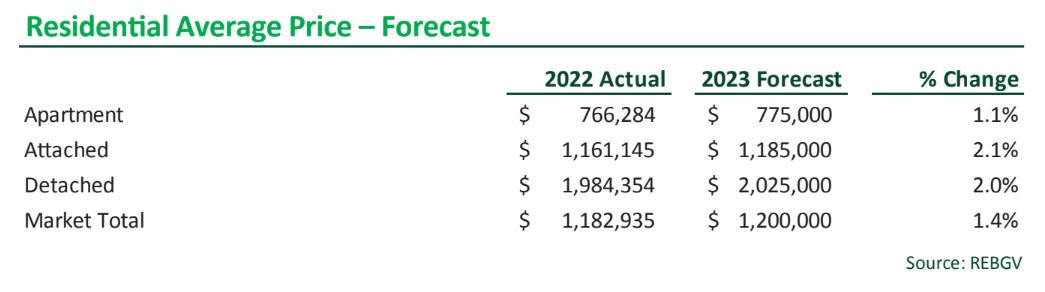

Home Price Forecasts

The average price across all product types for the REBGV area is forecast to reach approximately $ 1.2 million in 2023, which represents a 1.4 percent increase over 2022. Prices for apartments, attached and detached

homes are projected to increase in price by approximately one to two percent.

homes are projected to increase in price by approximately one to two percent.

The table below provides a summary of the price forecasts by product type:

Risks to the forecasts

At the time of publication, at least two reasonably foreseeable risks to these forecasts are worth noting:

1. Risk of economic recession

2. Risk of economic stagnation and higher mortgage rates

Risk of economic recession

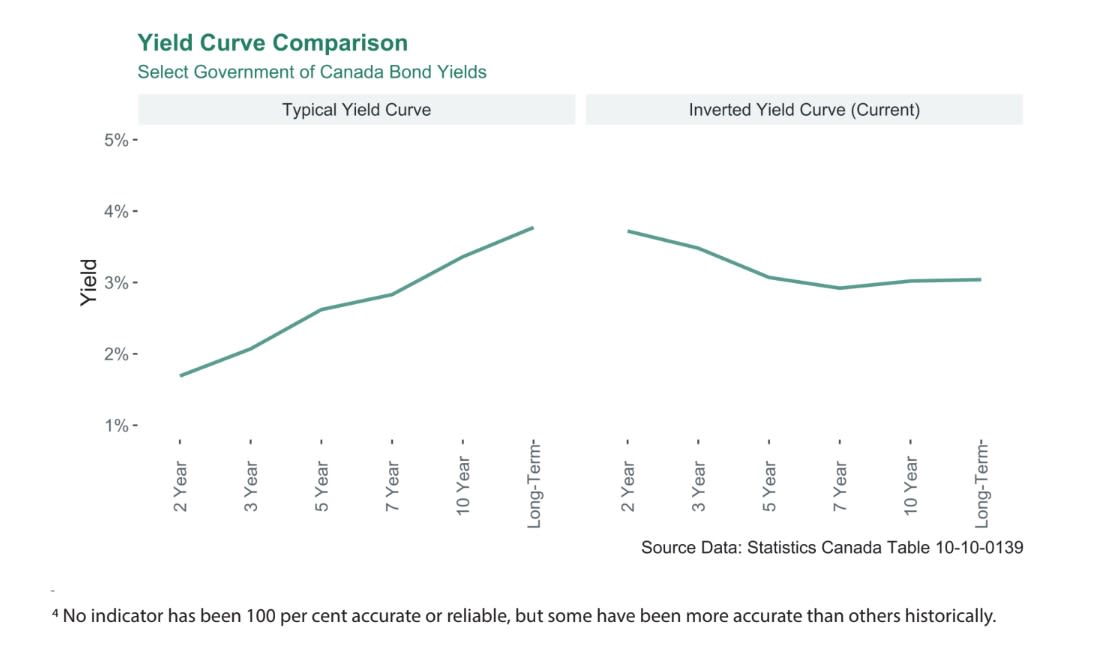

Economic recessions have historically been difficult to predict. This is because many of the factors used to identify recessions are usually only visible in hindsight, and often only many months (or years) after the recession has passed.An indicator often cited as being among the best* predictors of an economic recession is an inverted yield curve. Though it may sound complicated, the yield curve is simply a snapshot of the yields on government bonds of various maturities (i.e., one-year, two-year, three-year, five-year, etc.), taken at a point in time.

When an economy is functioning ‘normally; the yield curve typically slopes upwards, indicating that investors demand higher interest rates on money lent out for longer periods of time (i.e., the yield ona 10-year bond is higher than that of a 2-year bond).

Oftentimes before a recession, the yield curve “inverts” such that the yields on bonds with short-dated maturities become (temporarily) greater than yields on longer-dated maturities.

The oversimplified economic interpretation of this phenomenon is that investors are worried about the short-term prospects of the economy and are therefore demanding higher yields for investing money over short time horizons than over longer time horizons (when they expect the economy to eventually recover).

At the time of publication, the yield curve of both Canadian government bonds remains inverted and has been inverted for an unusually long period, historically speaking. While this does not necessarily mean a recession is imminent, it does represent a reasonably foreseeable risk.

The precise impact of a recession on the Metro Vancouver real estate market is difficult to predict since it largely hinges on the severity of the recession and the Bank of Canada’s policy response. Historically, when recessions have hit the Canadian economy with force (e.g., 2008/2009), the Bank of Canada has elected to lower the policy interest rate, which provides support to the real estate market in the form of lower borrowing costs.

Under the current scenario, however, inflation remains persistently higher than the Bank of Canada expected. This could make it difficult for the bank to reduce the policy rate significantly in the face of a recession, as this could cause inflation to continue to rise while the economy contracts.

Risk of economic stagnation and higher mortgage rates

Related to the risk of an economic recession alone, is the risk of economic stagnation (or recession) paired with a continued increase in interest and mortgage rates.

Among the most difficult scenarios central banks can find themselves in is one economist's term “stagflation”. This is a scenario where an economy is barely growing or is in recession, usually resulting in high unemployment, coupled with high inflation. In such a scenario, attempts of a central bank to rectify one situation can lead to exacerbating the other.

For example, a central bank choosing to increase the policy rate to fight inflation during a recession could lead to even greater unemployment. Conversely, lowering the policy rate to stimulate the economy while inflation remains elevated could lead to even higher inflation. It is a vexing problem, and no easy solutions exist. Ultimately, policymakers must make difficult choices between exacerbating inflation by trying to stimulate the economy or pushing up unemployment by trying to reign in inflation.

At the time of publication, this situation is fortunately not currently the case. However, given that inflation remains persistently elevated and other economic indicators (e.g., yield curve inversion, etc.) suggest economic trouble may be on the horizon, this potential scenario represents a reasonably foreseeable risk.

Summary of the downside and upside risks

Downside risks

With regard to the foregoing, downside risks to the forecasts are at least twofold:

1, Sales could slow more significantly than forecast if the economy stalls and heads into a recession.

2. Valuations could be lower than forecast if the recession is accompanied by significant job losses, and persistently high (or rising) inflation, leading to even higher costs of borrowing.

Upside risks

Upside risks to the forecasts are:

1. Sales activity and valuations could be higher than forecast if a recession is avoided and inflation declines more rapidly than expected, leading to meaningful reductions in the cost of borrowing.